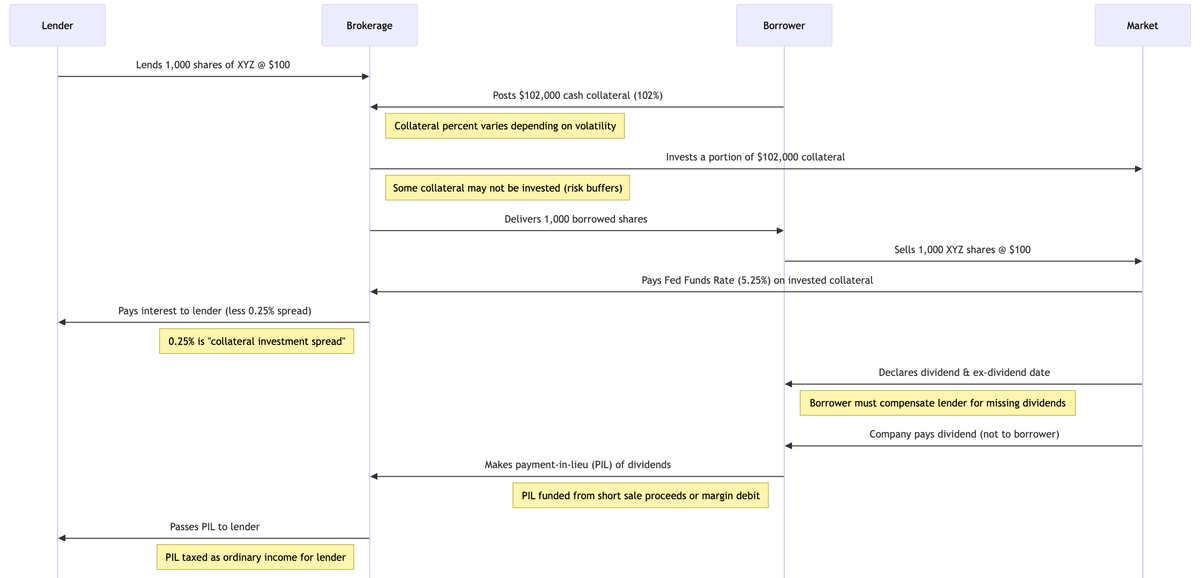

ETF Taxation Payment in lieu is taxing you Securities lending might mean paying more tax. Brent Sullivan· February 12, 2025 · 2 min read Sequence diagram of short-seller borrowing shares and owing the lender a poorly-taxed “dividend”

Sequence diagram of short-seller borrowing shares and owing the lender a poorly-taxed “dividend”

Sequence diagram of short-seller borrowing shares and owing the lender a poorly-taxed “dividend”