Option collar phantom income

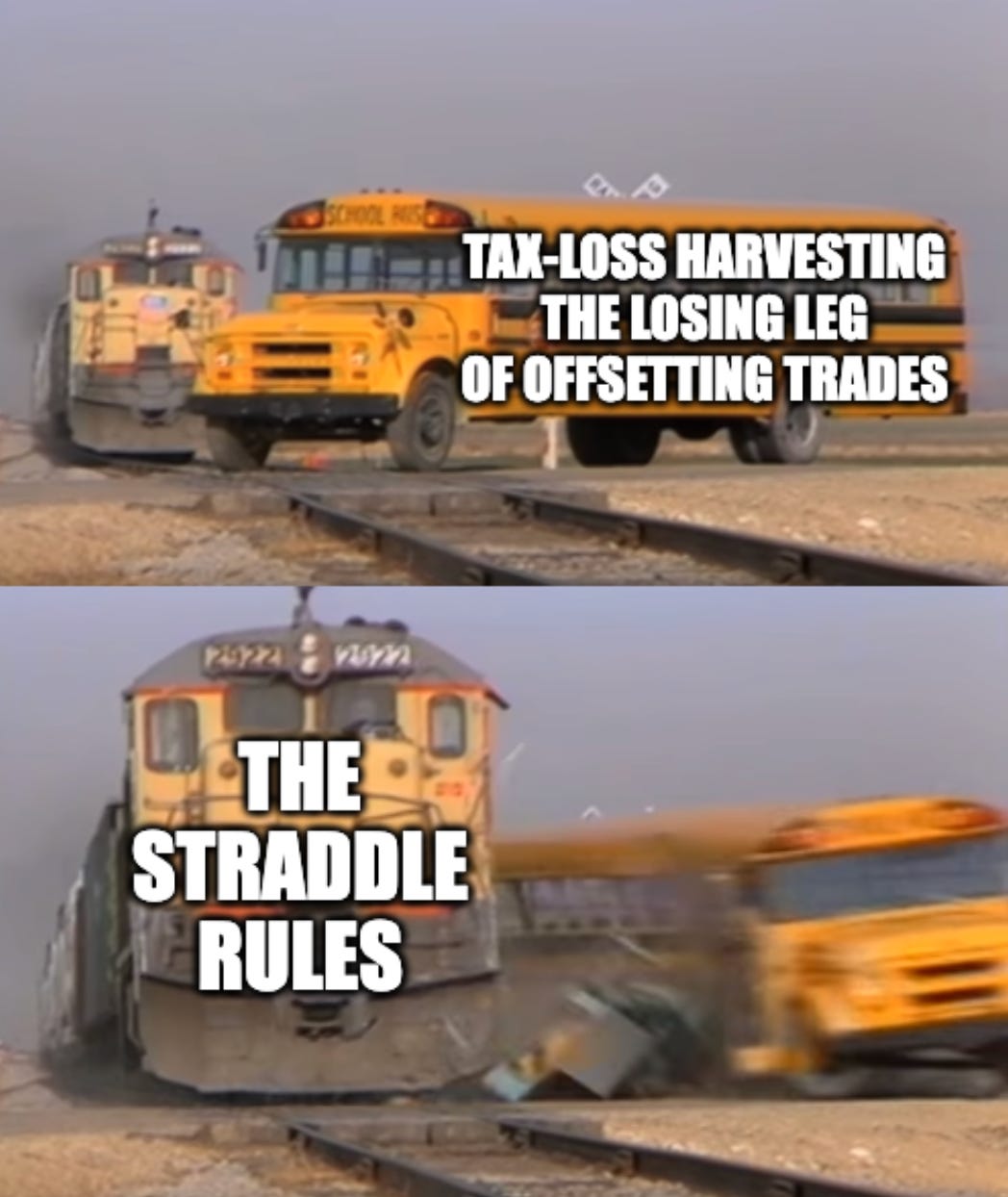

When the straddle rules kick in, note the (intended) tax costs

Basis Northwest is presented by Canvas (of Franklin Templeton)

Basis Northwest registration is open.

Early bird tickets will be gone very soon.

This article talks about the taxation of options contracts, but it is not investment, tax, or legal advice. There are many exceptions to consider in this area of taxation, and this article is far from comprehensive. Hire an adviser for personalized guidance.

The straddle rules were introduced in the Economic Recovery Tax Act of 1981 and were intended to curb some aggressive tax maneuvers in commodity trading.

The trade was essentially to hold two offsetting positions, harvest the losing leg before year-end, and defer realizing gain on the winning leg, thereby indefinitely deferring total portfolio net gain.

Congress ended that trade by introducing IRC Section 1092, the straddle rules. In 1984, Section 1092 was expanded to include options.

This is highly relevant nowadays.

Many concentrated stock solutions use options, explicitly (as in option collars) or implicitly (as in variable prepaid forwards).

Last week, I wrote about straddle rule basics using a covered call as an example.

This week, I’m doing a simple illustration of how loss deferral works (generally a bad thing) in an option collar.