Schwab: long/short "not a balance sheet capital-intensive type of activity"

Schwab's 1Q26 earnings highlight long/short repeatedly

Discounts for advisers, just reply to this email.

The agenda should be available by mid-next week.

Tax-aware long/short is all over Schwab’s 1Q26 results.

Getting up to speed on tax-aware long/short? Start here.

Before jumping in… plenty of folks have asked me about Elm’s write up on tax-aware long/short, which Matt Levine picked up.

I think Haghani and White are directionally correct on the importance of cost and complexity, but I’m not a fan of drawing precise results (e.g., “an average after-tax return of 2.16% pa” and “LSDI program’s expected return is 0.11% pa lower,” etc.) using an imprecise model like geometric brownian motion (GBM).

For reference, Rama Cont’s 2000 paper lists 11 “statistical properties of asset returns” (things like fat tails, vol clustering, gain/loss asymmetry, etc.) that GBM doesn't capture. Elm’s results are a function of a vastly oversimplified model (constant drift, vol, and correlation, log-normality, etc.) and its inputs, which don’t reflect reality the way a sampling and rolling-window approach with confidence intervals would.

AQR’s paper from March covers the interplay of fees and alpha rigorously. Even if I disagree with Haghani and White’s methods and assumptions, I think they’re right to scrutinize cost and complexity.

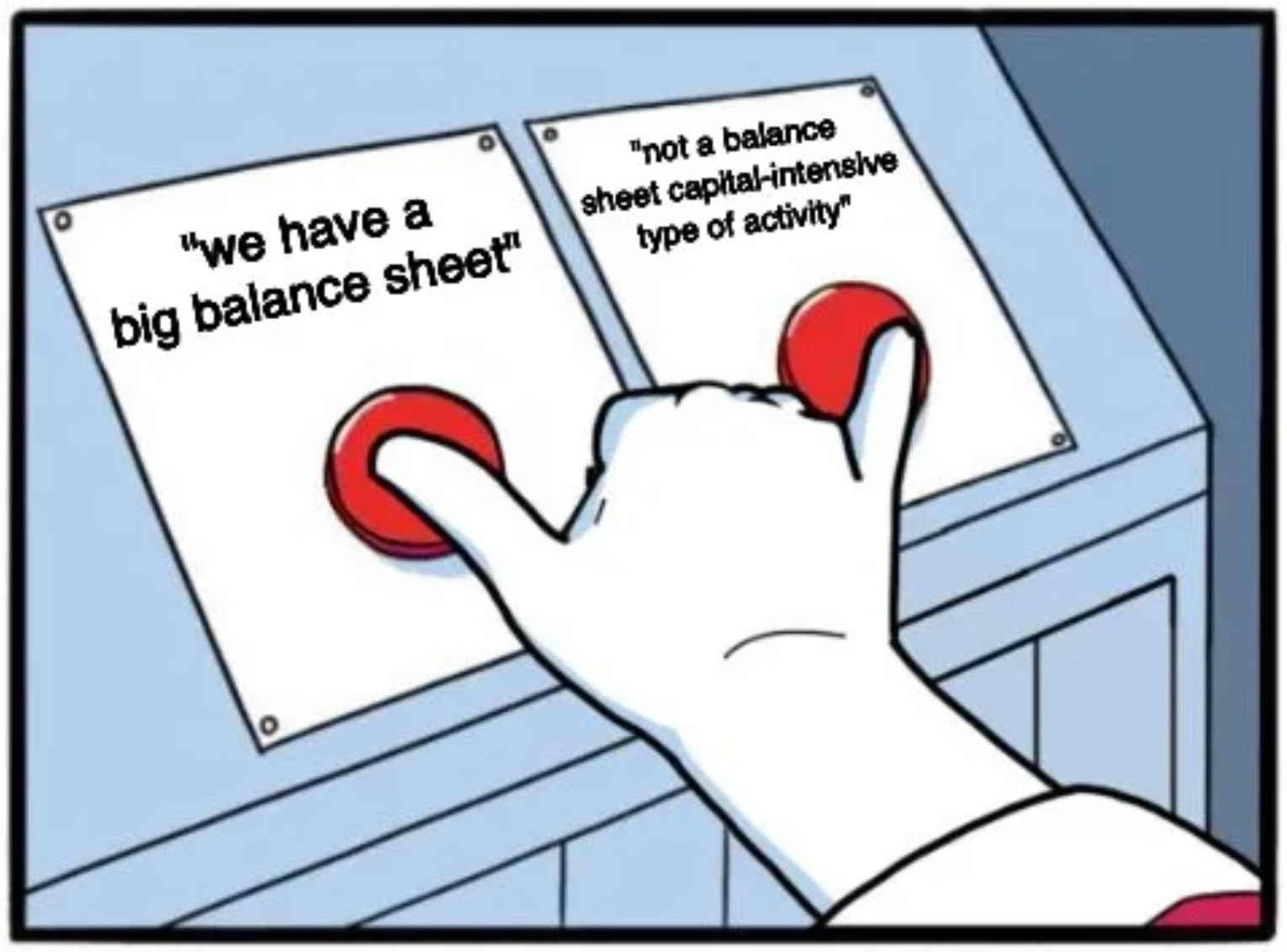

Just a month ago, Schwab’s CEO told us that they welcome advisers departing Fidelity due to rising financing rates and that they have a “big balance sheet” to support new long/short activity.

Then, on the 1Q Schwab earnings call last week, Schwab said that long/short is “not a balance sheet capital-intensive type of activity.”

The latter seems more correct.

Schwab’s numbers are interesting (“$21.3 billion related to long/short strategies implemented by RIA clients”), but I think investors and advisers are wondering whether Fidelity is raising rates for business reasons, to mitigate risk, or for some other reason entirely.

If long/short isn’t balance sheet intensive, what could be driving Fidelity to increase financing for some of its intermediary clients?