This is educational content. For tailored advice, consult an advisor.

Tax Alpha Bulletin Board

🦃 Annual subs to Tax Alpha Insider are 30% off through Cyber Monday 🦃

🎉 Basis Northwest: 2 days of taxable wealth innovation 👉 Seattle - May 2026

🔬 Call for papers: JWM Fall 2026 issue on concentrated wealth due Feb 1, 2026

Donate and deduct: AGI limit heatmap

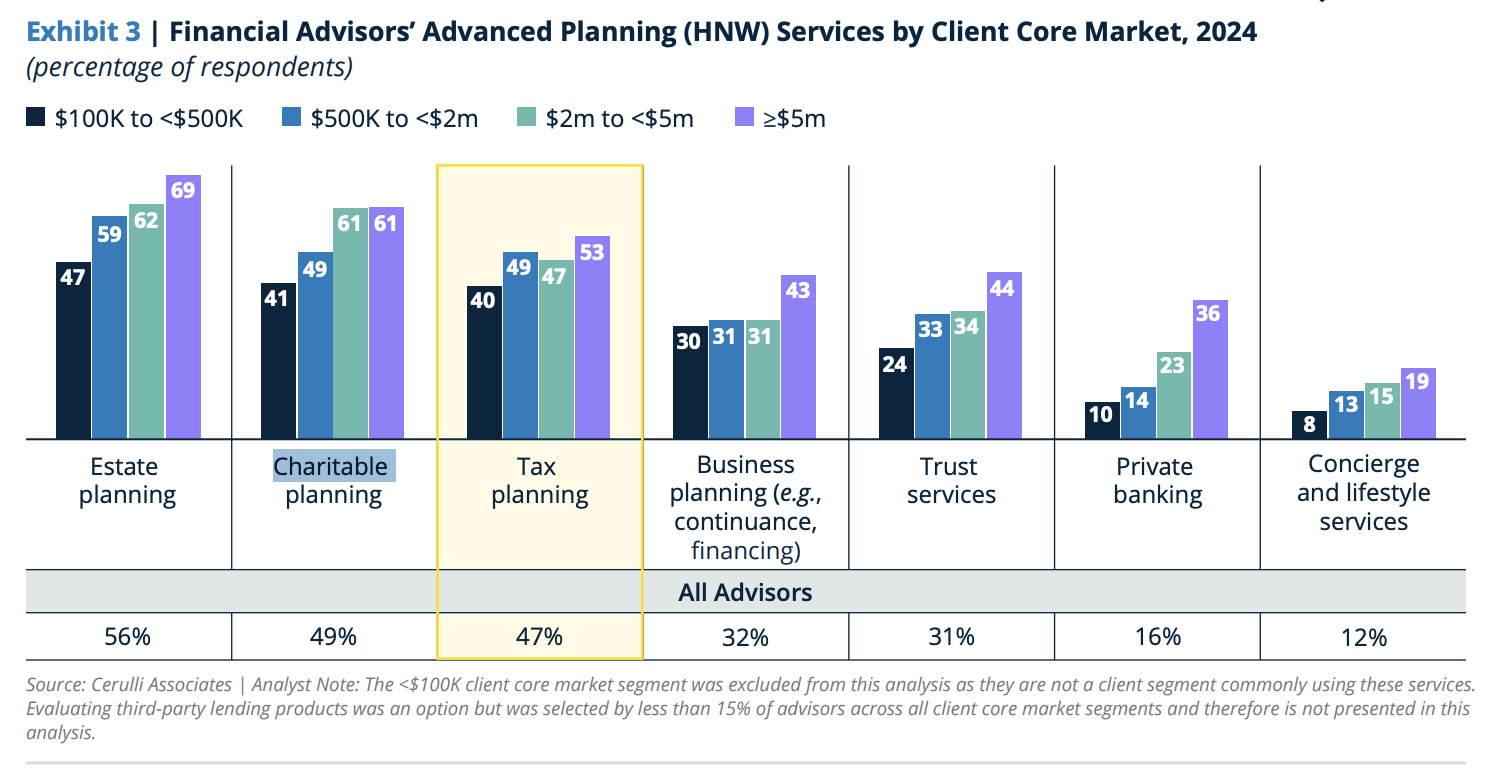

Cerulli’s latest Parametric-commissioned report shows that estate, charitable, and tax planning are among the top “advanced” services advisers provide, particularly for HNW clients.

While there’s some debate about centralizing those services…

…many see them as part of comprehensive wealth management.

Charity, namely the when/what/how to give to maximize donations and deductions, is a great opportunity for planners.

I recently teamed up with Morgan Stanley Investment Management on a philanthropy-focused continuing education course, arriving tomorrow, along with Brian Smith, Eileen Tam, and Tom Faust (former CEO of Eaton Vance and Chairman of Morgan Stanley Investment Management).

While prepping for that content, I needed to be able to quickly recall two important limits to deductions tied to charitable giving:

- Adjusted Gross Income (AGI) (IRC § 170(b))

- Deduction valuation (IRC § 170(e))

These rules are only relevant if the household has AGI to begin with and itemizes its deductions. They must also attach Form 8283 for noncash gifts above $500 to their annual tax filing.

Here’s a heatmap showing current AGI limits from 60% down to 20% based on the recipient type and property characteristics, among other factors.