This article is educational, not legal, tax or investment advice. It is not a recommendation to buy or sell any security. Hire an adviser for personalized guidance.

The evidence is overwhelming.

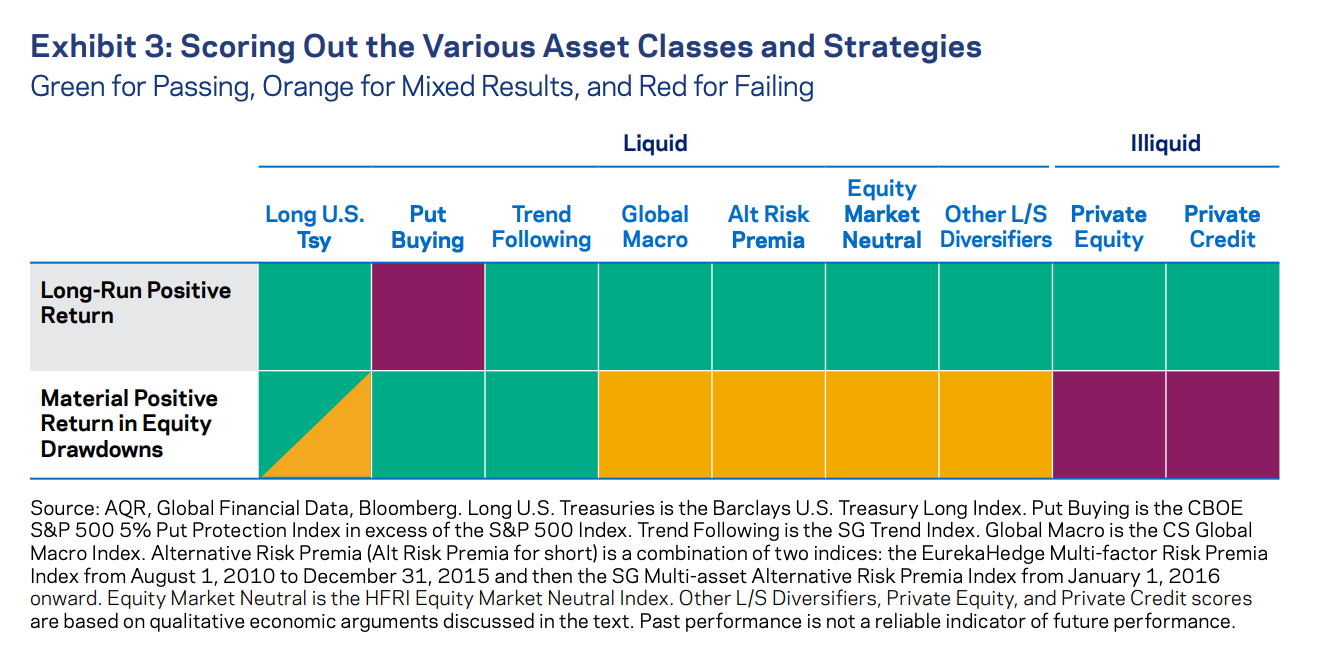

Managed futures deliver "crisis alpha" using trend following strategies across dozens to hundreds of markets consistently across decades, generally resulting in portfolios with higher Sharpe ratios.

"Crisis alpha" is consistent enough that some folks call managed futures a kind of insurance and make comparisons to other insurance-like strategies.

However... as with all insurance-like things, some folks, rightly or wrongly, aren't happy about paying for it when they don't need it.

I hear the same three complaints from allocators over and over.

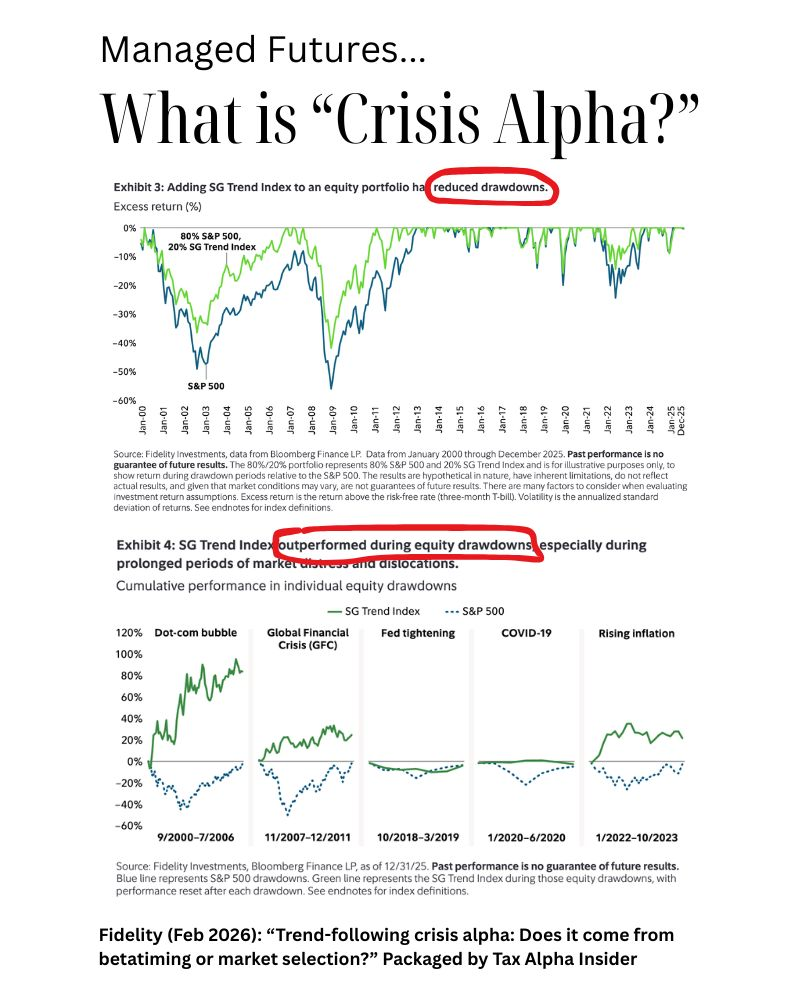

But first... what is "crisis alpha" and what causes it?

And can it be delivered tax-efficiently?

Fidelity put "crisis alpha" this way in a Feb 2026 paper...

They're essentially saying that managed futures is contrarian and able to reflect those views much more readily than cash securities (i.e. shorting a bond is hard, but shorting a rate futures is not).

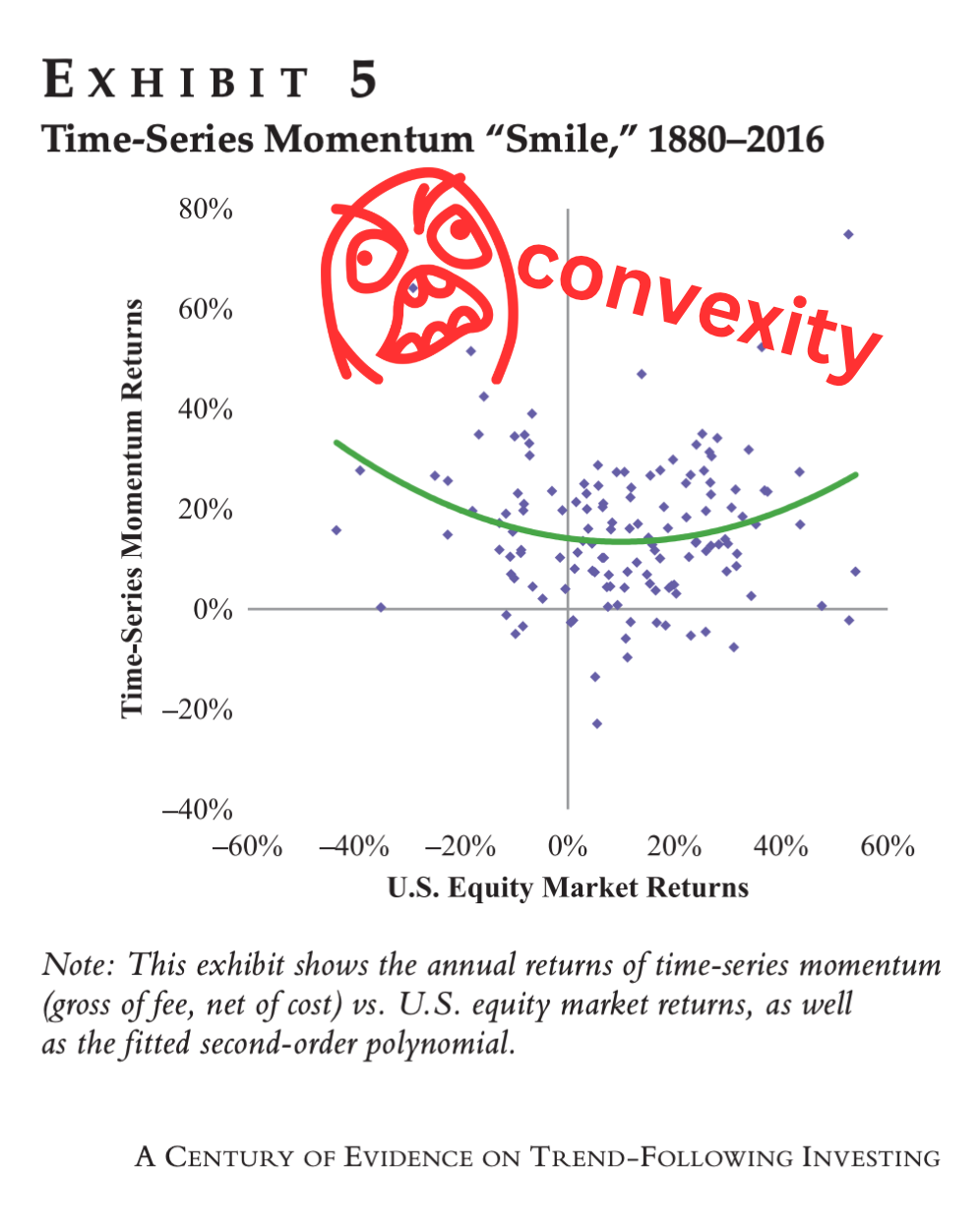

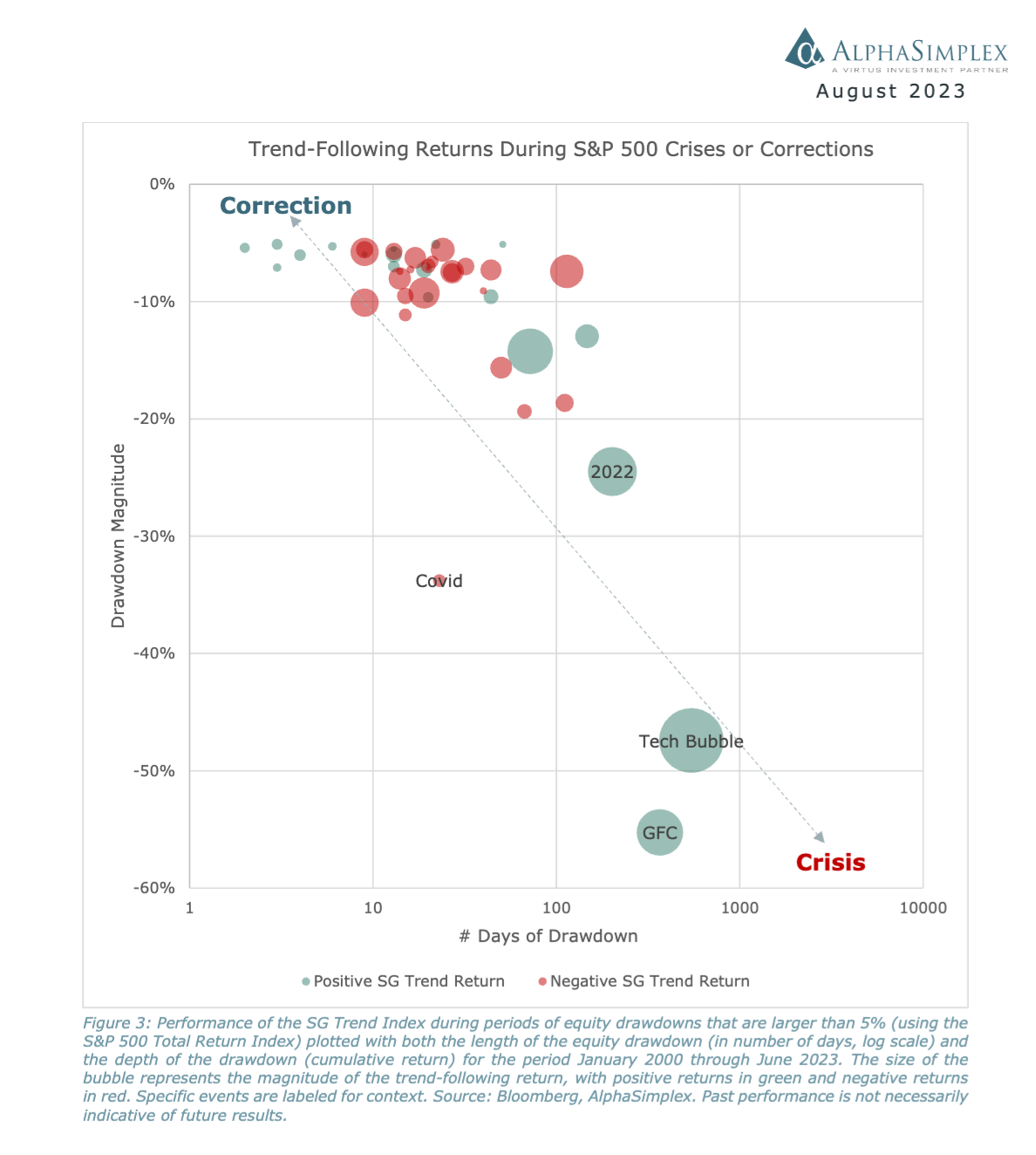

The 100-year trend paper I wrote about earlier this week suggests a "smile" that is perhaps the most quantitatively interesting phenomenon in managed futures.

Looking at the chart closely, the "smile" is the relative outperformance of time-series momentum versus US equity market returns.

This is the vaunted CONVEXITY that everyone in options portfolio construction drools over because it suggests better returns in some circumstances for the same amount of risk.

Does this always happen? No. There are some nuances around the type of crisis.

Namely, that trend-following strategies need a trend to latch onto: "Trend-following performance seems to be most robust during prolonged crisis periods; it tends to be mixed for equity corrections and generally negative for bond market corrections." (Kaminski 2023).

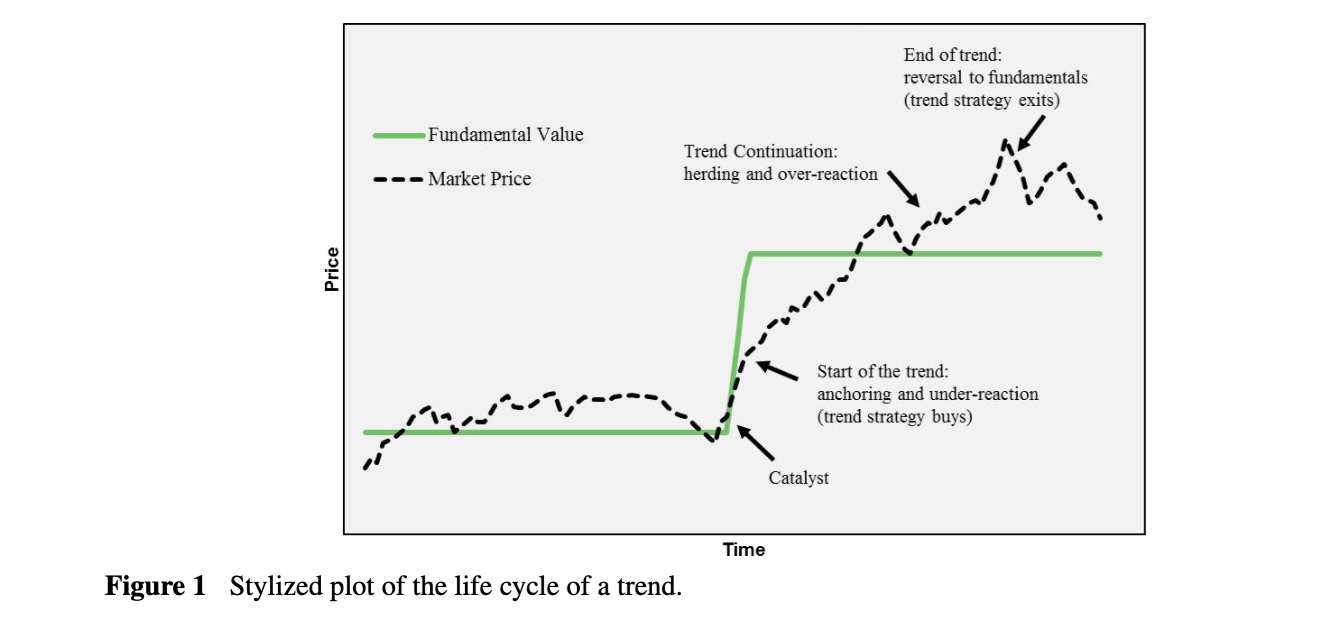

When it does happen, why?

- Start of the trend: Under-reaction to information

- Trend continuation: Delayed over-reaction

- End of the trend: Reversal

If people under/overreact in a sustained way, then while they're dumping risk assets and moving into safe assets, for instance, the trend is staring them down, and slowly pouncing.

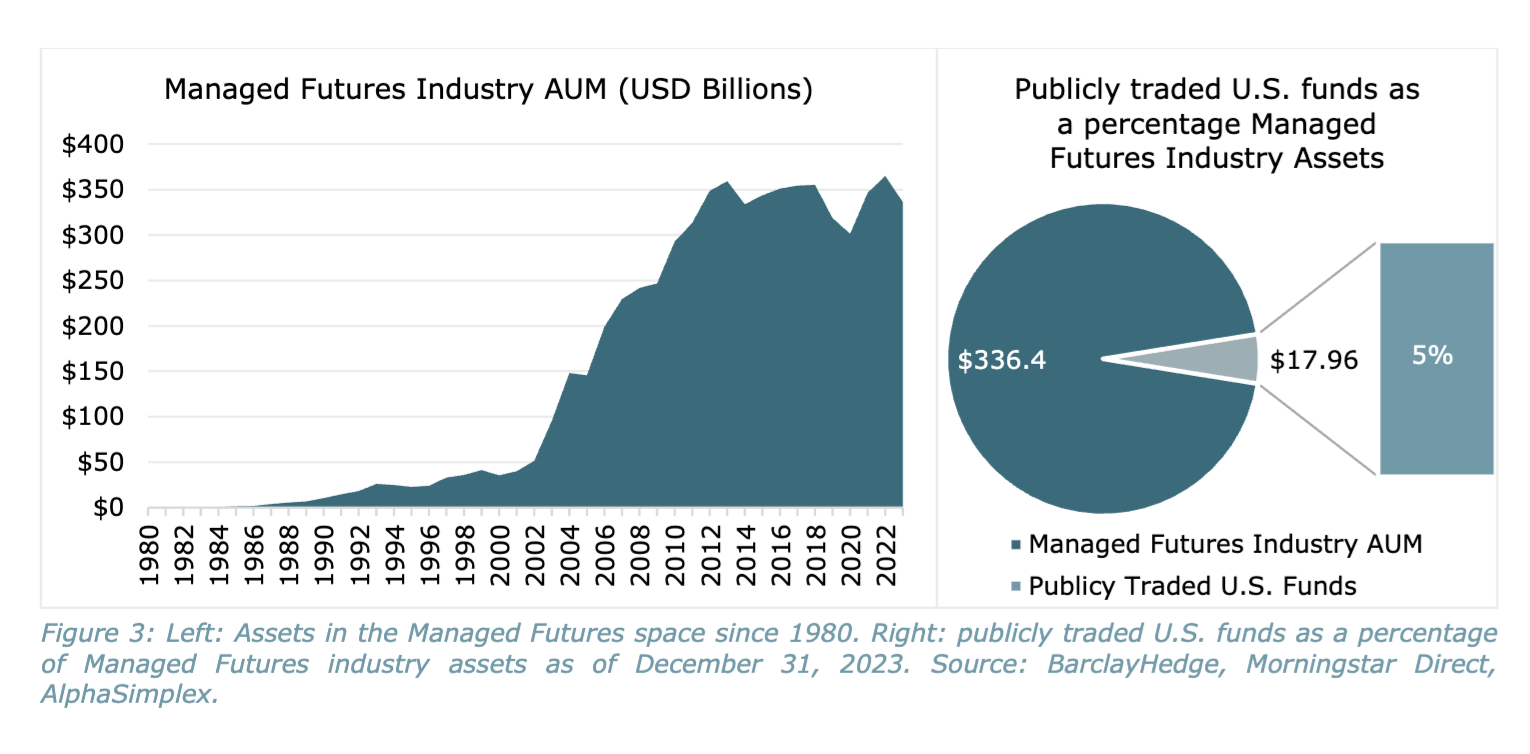

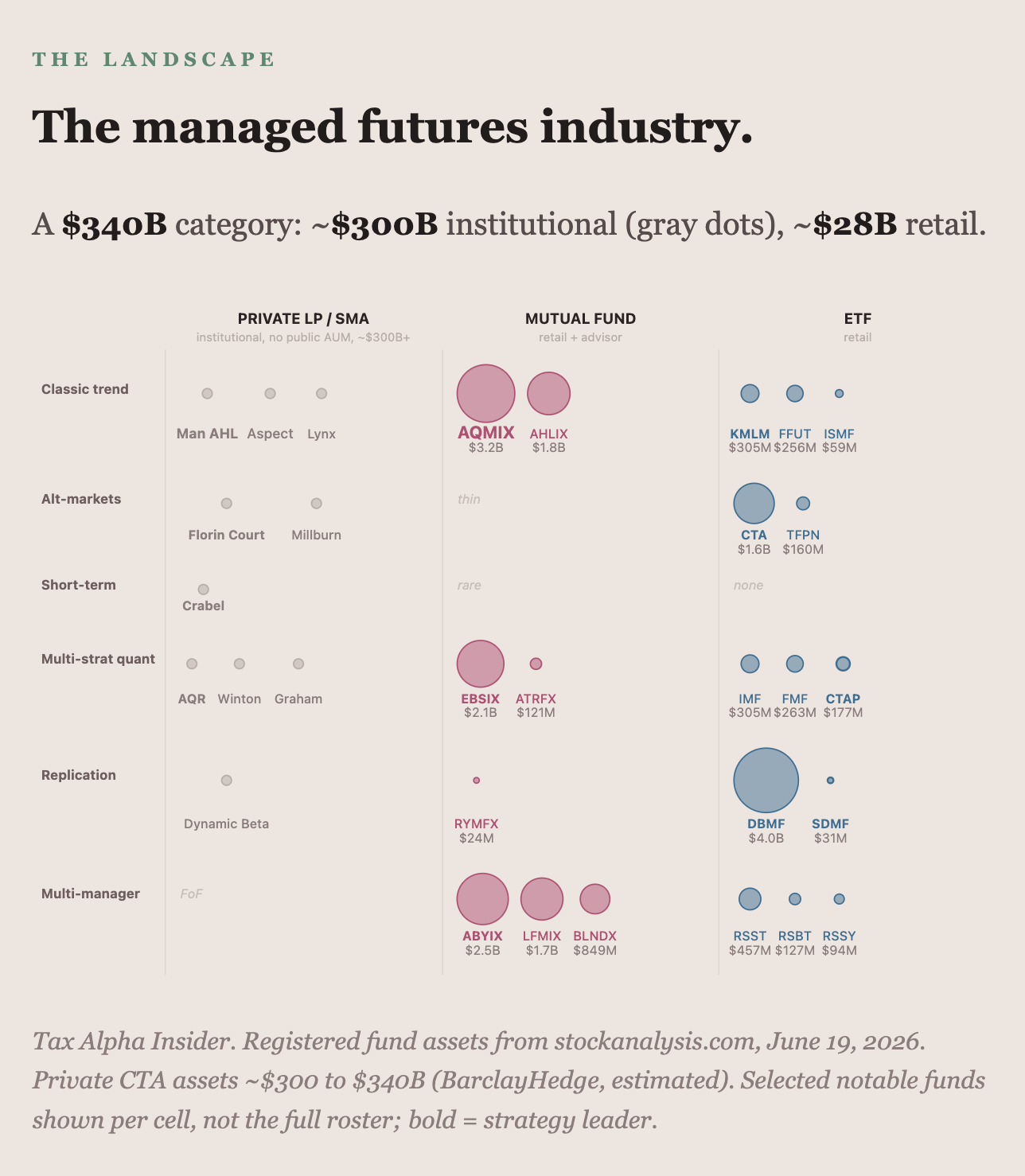

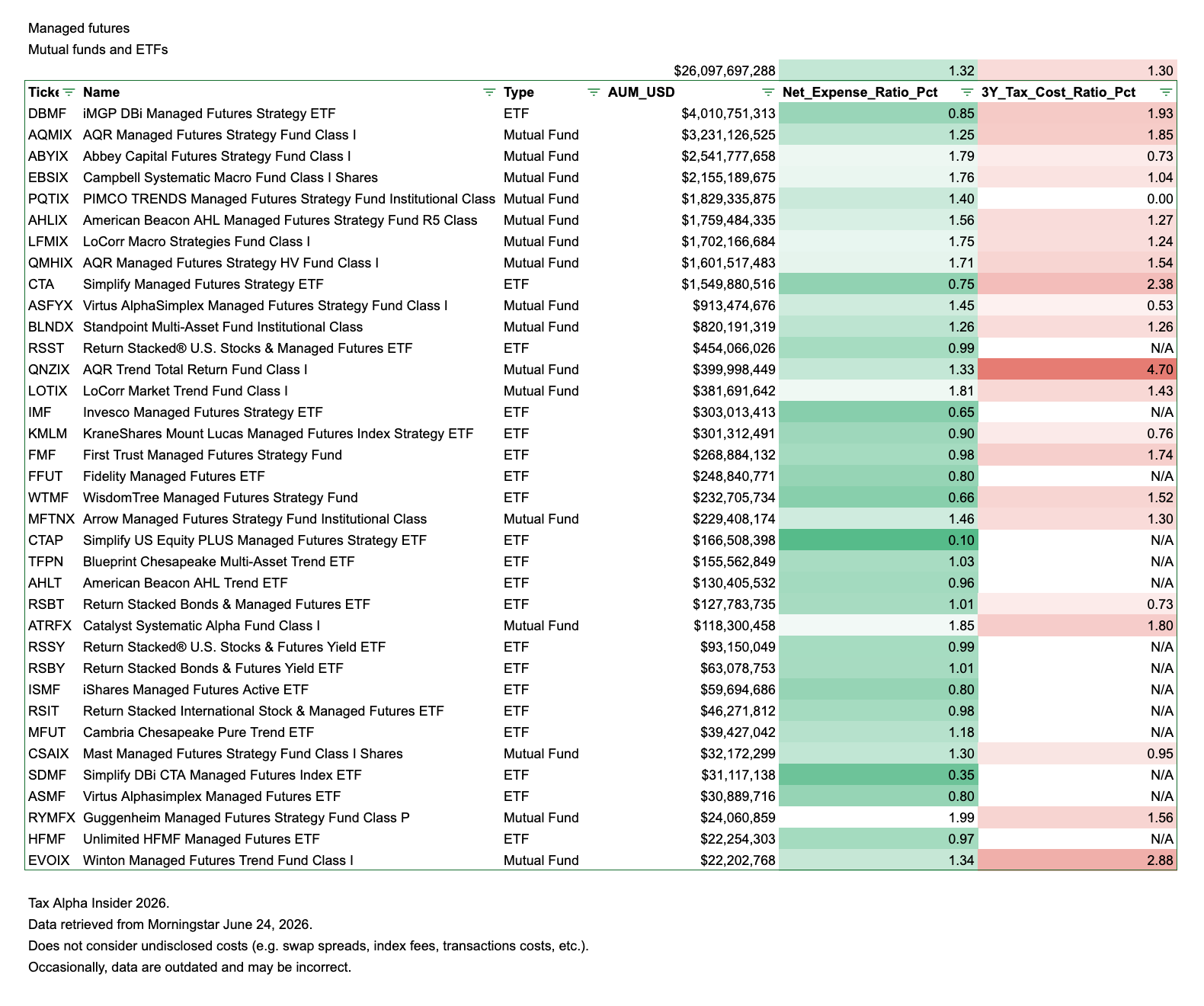

The managed futures world is ~$300bn AUM, with ~90% of that being institutional.

Here's a bit more granularity...

Why is that if the results are so compelling?

It's probably some combination of the following:

- It's not intuitive ("it's not beta, it's not duration... what is it?")

- Relatively high net expense ratios

- Relatively high tax cost ratio

Developing intuition takes some effort. That's a lift, but a comparatively low one.

No one likes higher costs, and no one likes explaining higher costs to clients. And I'd guess that sticker shock is stopping some folks from doing the deeper work to form intuition that shows there's meaningful value here.

To help with the sticker shock, there are some efforts underway involving swaps and long/short. That's a work in progress, but those pieces should land next week.

p.s. Things will slow down for the next two weeks as I head to upstate NY with family (Cooperstown) and then NYC for 2 days with my oldest son for a podcast recording and NYM game.